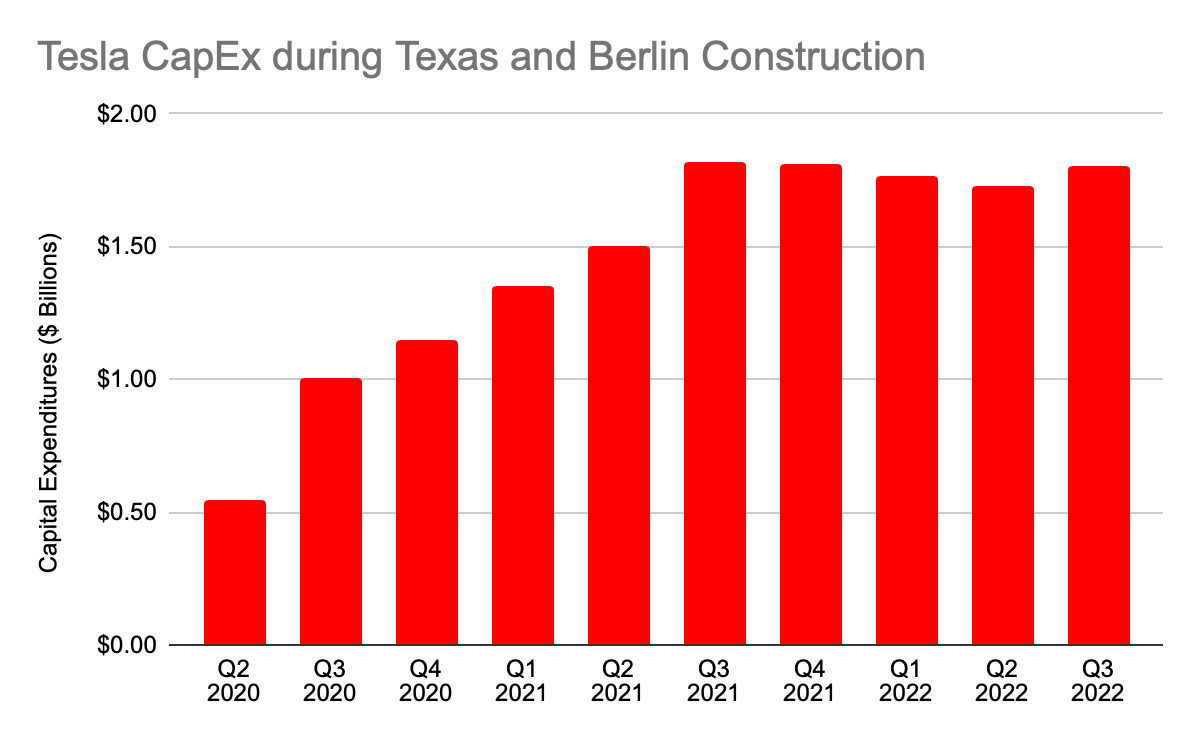

Tesla had $12.7B total cumulative capital expenditures invested across their entire enterprise between Q2 ‘20 and Q2 ‘22.

During this time period, gigafactories for making Model Ys in Berlin, Germany and Austin, Texas, USA were constructed, permitted, brought into low-rate initial production and reached roughly breakeven rate of cash flow, thus ending their investment phase. As of Q3 ‘22 these factories are making positive gross margins and may be close to breakeven overall. If not, they almost certainly will be making good money by the end of Q4 when they reach volume production of around 5k cars per week, according to Tesla management guidance.

Tesla’s Master of Coin and CFO Zach Kirkhorn said on the Q3 earnings call:

“Note that while small and growing, each car we build in Austin and Berlin is contributing positively to profitability.”

$12.7B to build two gigantic cutting-edge car factories in just two years would already be a pretty good deal, but there were also substantial capital expenditures in other areas, such as:

Shanghai and Fremont, which tripled their combined output in those two years

Lathrop factory for Megapacks

Research and development

Supercharger network doubling from 2,035 locations / 18,100 stalls to 3,971 locations / 36,165 stalls

Store and service center network expanding 59% from 446 locations to 709

Mobile service fleet expanding 89% from 769 vehicles to 1,453

So, $12.7B is an upper bound for how much startup cost might have been involved in creating the gigafactories in Berlin and Texas.

Pessimistic Baseline Case

Let’s start conservatively with assuming that $10B was the total CapEx directly attributable to Berlin and Texas, and that this was only enough to achieve the nominal 250k annualized run rate for the production capacity currently installed.

$10B invested / (2 * 250k cars/yr) = $20k investment per car of annual capacity.

In Q1 '22, before Berlin and Texas expenses started hitting automotive cost of goods sold, Tesla with Fremont and Shanghai did:

$4.86B auto gross profit / 310k deliveries = $16k global average gross profit per vehicle delivered.

(This is excluding zero-emission vehicles credit sales).

If Berlin and Austin merely match the unit economics of Fremont and Shanghai’s performance in Q1:

500k deliveries * $16k profit = $8B profit/year.

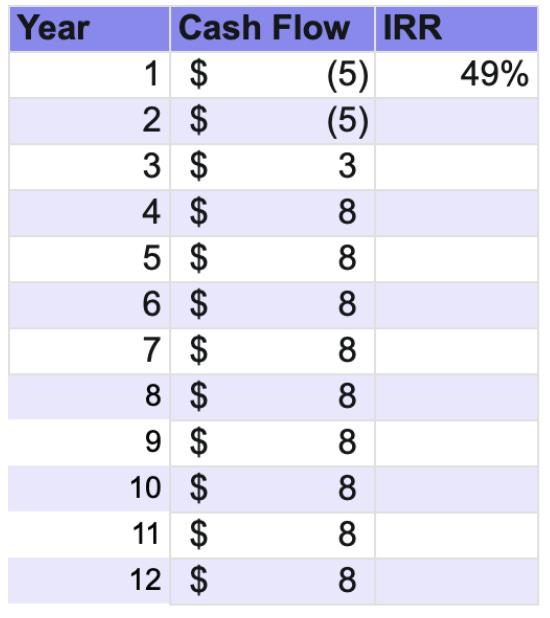

If we model the factory as needing a few quarters to ramp up and reach this level of production and profitability per car and then lasting 10 years before needing new investment, the cashflows look something approximately like what’s shown in Table 2 below. The factory would break even in just under two years of operation and the internal rate of return overall would be a whopping 49%.

The IRR estimate is not very sensitive to the expected lifetime. If we model even more conservatively for a five-year life before needing a bunch of new investment, it’s still giving a 41% annualized return on investment, because an IRR this high comes with severe discounting on years that far into the future.

A More Likely Scenario

Now let’s model for lower CapEx estimates for Berlin and Texas and some improvement in profitability over Fremont and Shanghai’s performance in Q1 ‘22.

Capex:

$4B invested for each factory (or $8B combined)

Meaning that Tesla would have spent about 60% of its $12.7B total CapEx on Berlin and Texas

Additional $1B incremental investment in each factory will get them up to 500k/yr each, or 1M/yr combined

Total: 2 * ($4B + $1B) / 1M = $10k investment per car per year of capacity.

Gross Margin:

Probably closer to $25k per car on average in the long run

Roughly 40% gross margin if the average selling price is $63k

The minimum list price for a new Model Y in the United States is $66k right now, so using $63k as the estimate implies that prices will come down, probably due to reintroduction of a standard range version.

Cost savings from the latest and greatest design of the vehicle and factory

Giga Texas in particular will be the beneficiary of huge US clean energy subsidies

About $3.5k on average for manufacturing the battery

$7.5k consumer tax credit on the buyer’s side

Probably will tend to push Tesla’s average selling price higher either via raised prices increased take rate on upsells like red paint or a tow hitch

$11k of total federal subsidy affecting the economics of the American Ys

In this new model, the factories will have paid for themselves in about a year and a half of operation, and shockingly the IRR is 100%, as illustrated in the cash flow graph at the beginning of this article.

It could get even better

$25k per car may sound extremely high, but that could be done with average revenue per car of $63k and average cost of $38k. Given the historical costs for Model Y, the upcoming improvements from Berlin and Texas, and the actual list prices on Tesla.com for Ys, there’s a decent chance we might see more like $30k gross profit on $65k revenue and $35k cost.

Also, maybe the new factories cost even less than $4B. Maybe it was $3B, or at least maybe $3B is representative of Tesla’s construction costs for future production capacity, which is really what matters more over the long term.

If so, the IRR jumps to 123%

To be clear, I can't estimate any of this precisely.

How fast the factories ramp

How much CapEx actually was spent, or more importantly, how much will be spent on future capacity

How long the equipment will last or how much it will cost to keep it up and running over the years

How much gross profit will be earned per car

Nevertheless, with such an extreme result it doesn't even matter for practical purposes, and if I have managed to avoid systematic bias then the random errors more likely than not will roughly cancel out. Even the low-end 40% estimate is a fantastic return on investment.

I don't know of any other business in any industry that can generate return on investment like this with such low risk. It's not like this is some speculative, high-risk-high-reward moonshot venture, like we might see in biotech or pharmaceuticals. This is just for building out more production facilities for Model Y, the most popular car ever designed.

I am about 99.9% all-in on Tesla via TSLA stock and call options. These are notes for my model that I’m sharing. I fully believe what I have written and I’ve put all of my money where my mouth is, but this is not advice regarding your personal investment or financial decisions. I'm not a certified professional investment or financial advisor and even if I were one, broad buying or selling advice would be inappropriate because there are so many variables to take into consideration such as your goals, risk tolerance, financial outlook, income, age, tax situation, dependents, and so on. Make your own choices. I hope one of those choices is to share this article with everyone you know, but that’s up to you. Thanks for reading.