Tesla vs. Top Megacaps: Smackdown Round 2

Head-to-Head Trend Chart Face-off and Market Cap Implications

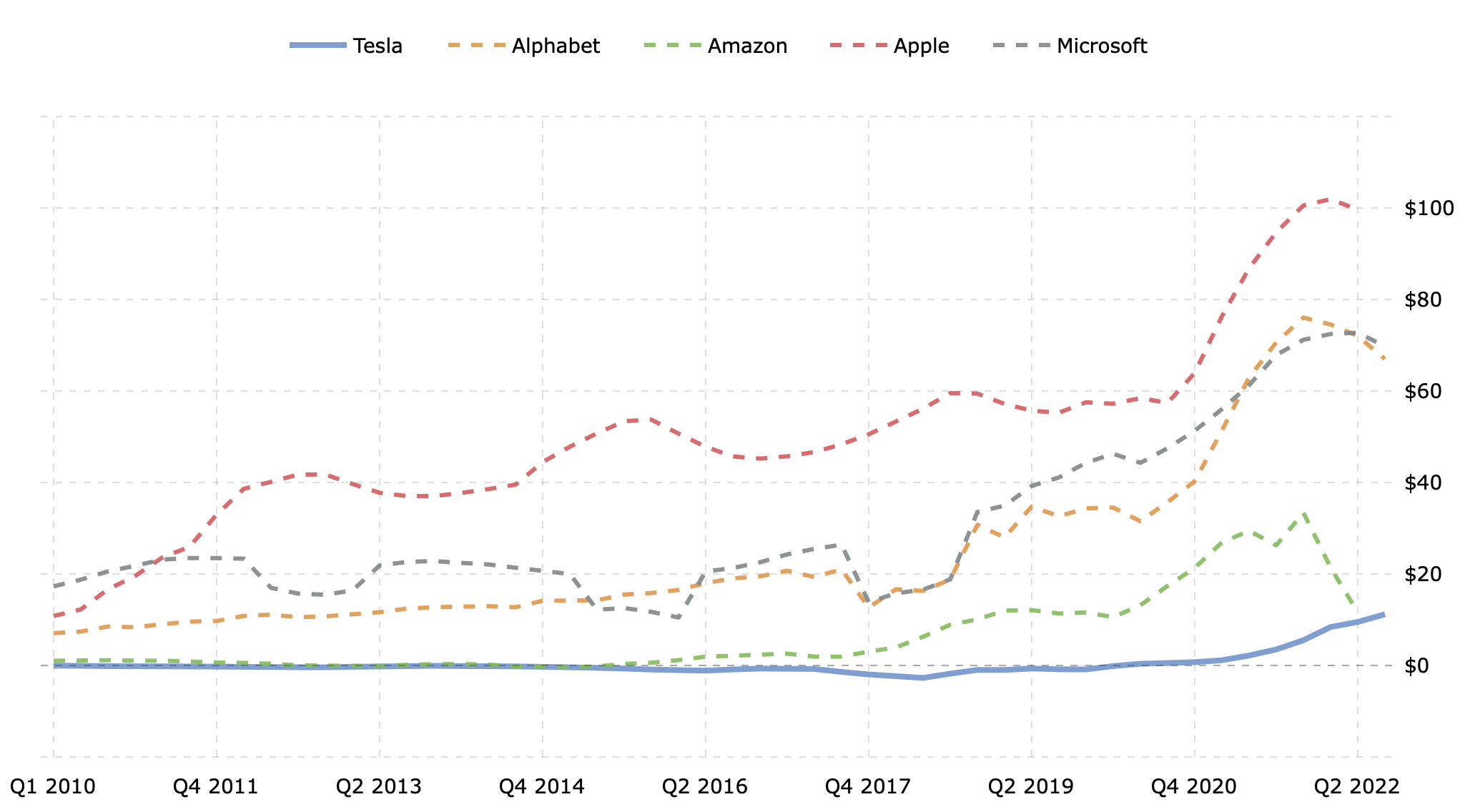

Net Income

Tesla with the highest compound annual growth rate and about to pass Amazon soon

Only Tesla has been growing income since 2021

Operating leverage starting to kick in hard, and will be growing substantially faster than revenue for the next few years

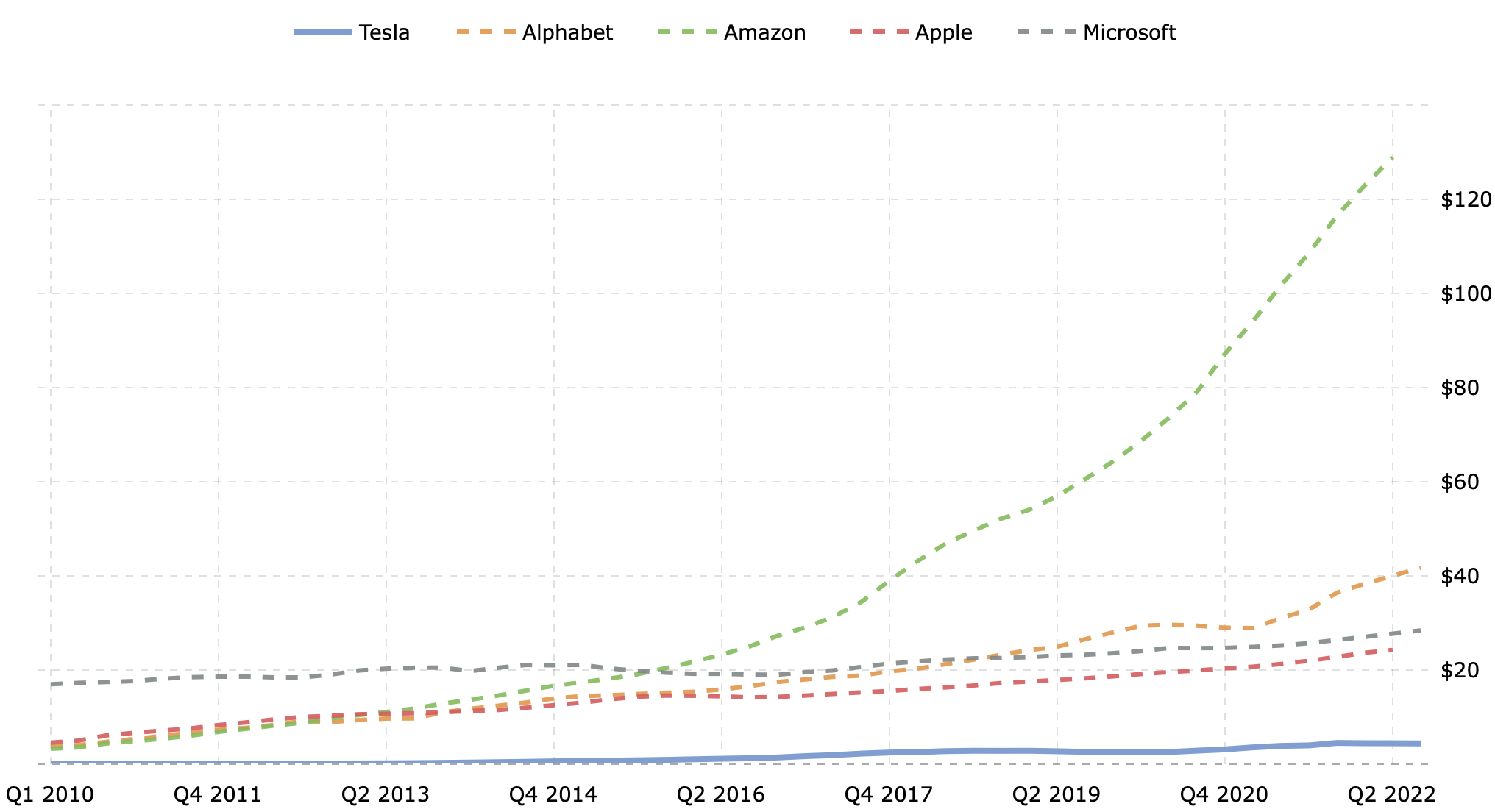

Revenue

Tesla once again with the highest compound annual growth rate

Tesla growth continues to inflect up since 2022 while all others inflected towards flattening out

Research & Development Expenses

Tesla is spending 9x less than next-closest Apple and Microsoft

Amazon doesn’t report R&D specifically but has very broad category for “Technology and Development” so their figure isn’t exactly comparable to the others here

Selling, General & Administrative Expenses

Tesla is spending 6x less than next-closest, Apple and Microsoft

Amazon figure includes order fulfillment costs, which was $21 billion in Q3 2022 alone

Long-Term Debt

Tesla has 7x less than next-closest Alphabet

Tesla’s debt is almost entirely tied to vehicle and energy product financing and is non-recourse debt

Tesla has $0.06B of debt not tied to this category

Gross Margin

Tesla lowest right now, but has fastest improvement trend and probably is headed towards around 40% a few years from now

Selling hardware instead of mainly software is the biggest factor

Matching Microsoft’s 70% margin is not going to happen unless Tesla solves autonomous driving and that becomes the main business

Fastest improvement trend

Gross margin on core automotive business is closer to 33%

Gross margin is not everything

As long as it’s high enough to indicate strong pricing power and protect from market downturns, then what matters most is revenue growth and operating leverage, both of which Tesla has in abundance

Tesla Compares Favorably

Currently smaller than all of the other four Big Tech giants, but best growth and prospects for future growth

Highest compound annual growth rate

By a wide margin

Consistent long-term exponential trend

Explicit management guidance for similar exponential growth moving forward

Extremely lean operating structure for R&D and SG&A that is an order of magnitude less expensive than

Only big tech company demonstrating ability to grow revenue quickly without increasing OpEx

Lower gross margins, but still excellent, improving, and with plenty of room in total addressable market to make it up in volume

Tesla has just 2% share of global car and light-truck market right now

~300 Terawatt-hours (TWh) of batteries needed in total to transition humanity to sustainable energy and get off fossil fuels

~20,000x more than Tesla’s current annual sales of batteries across both automotive and stationary storage businesses

Tesla targeting 3 TWh/year production by 2030

Tesla has a clear path to earning around $200B per year just on automotive business

Scale production 10x, get operating leverage

Would happen at roughly 15-20M cars/yr at $13k-$17k net profit per car

At 50% CAGR —> Around 2028

At 30% CAGR —> Around 2031

Official 2030 aspiration is 20M cars produced

Tesla comes with bonus options that could make trillions of dollars of profit per year if successful

Autonomous driving

Humanoid robot / Optimus

It’s early in the growth story for Tesla.

As long as they can continue to improve gross profit per car toward $20-25k for 35-45% gross margin and maintain reasonably tight control of operating expenses, then when they’re delivering 5-6 million cars per year their annual net income will pass $100B. With 50% annual production growth and a current annualized run rate of about 1.8 million cars/year, Tesla would reach reach this level of income in 2025.

Tesla $100 billion net income around 2025

Apple is currently valued at $2.4T with $100B net income, for a 24 P/E ratio, with low growth of revenue and earnings and operating expenses rising quickly.

Saudi Aramco also has earned about $100B on average over the last five years and has a similar market cap at $2.0T.

So, both of the only publicly traded companies that have ever achieved $100B annual earnings are worth at least $2T, even in the current bear market.

If Tesla were to achieve $100B net income while still explosively growing, the P/E ratio would probably be much higher than 24. Today it’s about 70 for TSLA, and that’s the lowest it’s ever been, due to eight consecutive quarters of compression from steady earnings growth.

Even if TSLA had a 40 P/E ratio at $100B earnings, that would imply a market cap of $4T and a share price of about $1,150, 5x higher than today’s closing price of $228.

If that happened by this time in ‘25, then the annual return on investment would be 70% for TSLA stock purchased today.

I am about 99.9% all-in on Tesla via TSLA stock and call options. These are notes for my model that I’m sharing. I fully believe what I have written and I’ve put all of my money where my mouth is, but this is not advice regarding your personal investment or financial decisions. I'm not a certified professional investment or financial advisor and even if I were one, broad buying or selling advice would be inappropriate because there are so many variables to take into consideration such as your goals, risk tolerance, financial outlook, income, age, tax situation, dependents, and so on. Make your own choices. I hope one of those choices is to share this article with everyone you know, but that’s up to you. Thanks for reading.