Tesla vs. Top Megacaps: Hardcore Smackdown

One of these things is not like the others...

Tesla’s car output has grown 60% annually for a decade straight with company guidance for 50%+ growth for the foreseeable future.

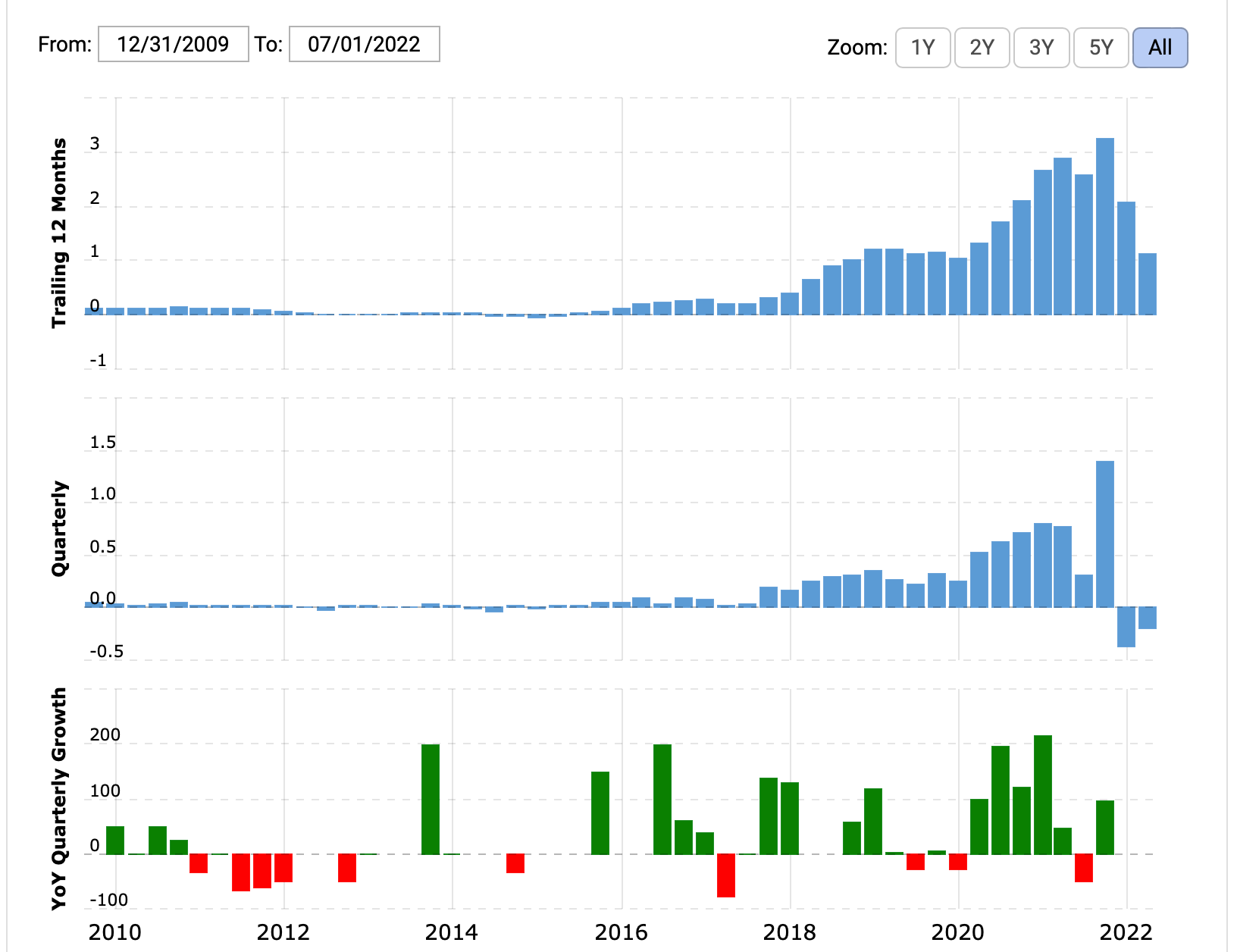

Tesla’s net income reached a critical tipping point in 2020 and since has been growing exponentially along with production volume.

Tesla’s earnings per share growth has compressed the trailing twelve month PE ratio from 1100 to 70 in just two years.

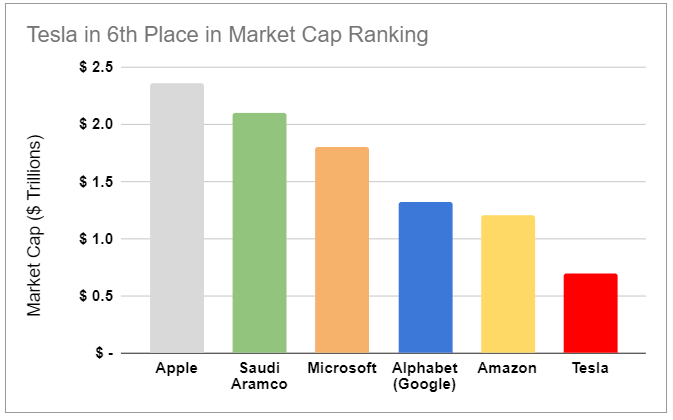

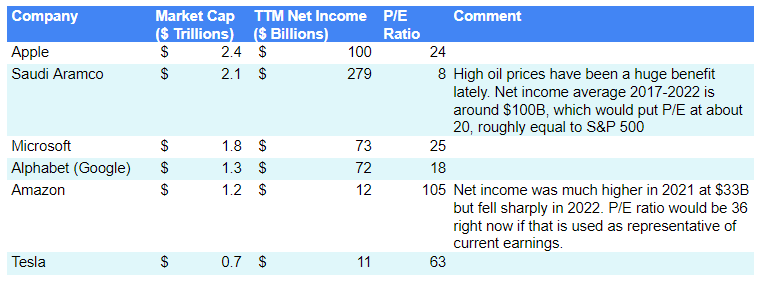

Should Tesla Be #1 on the Market Cap Ranking?

For some context before we begin, consider Technoking of Tesla Elon Musk’s recent comments on the Q3 2022 Tesla earnings call:

We have our sort of local ups and downs, but the long-term trend has been extremely good. And several years ago, I said, I think on our earnings call, that I thought it was possible for Tesla to be worth more than Apple, which was then the highest-cap company, I think, in the market. At that time, I think it was around $700 billion. And I said it required an incredible execution, at least some luck, and we didn't only achieve that.

Tesla went — in fact, surpassed Apple's market cap at the time. And now, we have the opinion that we can far exceed Apple's current market cap. In fact, I see a potential path with Tesla worth more than Apple and Saudi Aramco combined [$4.5 trillion]. So now, that doesn't mean it will happen or that will be easy.

In fact, I think it will be very difficult. It will require a lot of work, some very creative new products, manage expansion, and always luck. But for the first time, I am seeing — I see a way for Tesla to be — let's say, roughly twice the value of Saudi Aramco. And I think that's — I haven't quite seen that yet.

I mean this is the first time I've seen that potential. So, we have an incredible product portfolio. I think we've got the most exciting product portfolio of any company on earth, some of which you've heard about, some of which you haven't.

Let’s look at the business fundamentals and demonstrated financial performance of each of these six companies.

As it turns out, the numbers for Tesla are drastically better than any company ever in the entire history of formal commerce since the ancient Mesopotamians first invented the concept of money 5,000 years ago.

Usually things that sound too good to be true are actually false, especially when money is involved, but there are rare exceptions…

Apple

Apple Revenue

Apple Earnings per Share

Apple Gross, Operating and Net Margin

Apple Notes

Net income now $100 billion per year

Strong, steady, uninterrupted earnings for more than a decade straight

Brutally strong competitive position, pricing power and unit cost control, yielding outstanding gross profit margins now over 40%

Services margin is around 70%, but only 25% share of overall revenue

Arguably the strongest brand in the world

Loyal, cult-like fanbase locked into seamlessly integrated software and hardware ecosystem, many of whom won’t even consider buying from competitors

Substantial amount of vertical integration of hardware, software and services, and the key strategic move announced in 2020 to design custom computer chips such as the M1 seems to be working out well thus far

“People who are really serious about software should make their own hardware” - Steve Jobs, quoting Alan Kay in the iconic 2007 iPhone reveal

Mediocre growth since 2012

2021 was the only year since 2012 with *any* significant earnings growth

2012-2020 net income saw a mere 5% compound annual growth rate (CAGR), same as the S&P 500

This happened mainly due to margin expansion from higher pricing on iPhone 12 and 13 compared to previous generations, and it’s unclear to me how sustainable this is, but I’m not especially familiar with the details of Apple’s business

Since 2014, revenue has doubled for a 9% CAGR

Majority of revenue comes from iPhone, Mac and iPad; no new major revenue streams or breakthrough revolutionary products in the last decade

iPhone alone is half of company revenue

Operating expenses for research & development and selling, general and administrative now costing $50 billion per year and linearly increasing by $4 billion per year

Optimistic best-case total addressable market (TAM) of core personal electronics business of very roughly $5 trillion revenue

If average revenue is $1k per customer per year for personal electronics and there are 5 billion customers someday (about half of all humans alive in 2050)

Would yield $1 trillion annual earnings at 20% net margin, for 10x growth from today’s earnings

Possible opportunities exist for Apple to expand their TAM by stepping into markets outside personal electronic devices, by leveraging their cash, talent pool, retail footprint and brand

Saudi Aramco

Aramco Notes

Sells mainly two commodity products, oil and natural gas, with inelastic supply and demand affected by a multitude of random factors

Wildly variable and unpredictable prices

For Aramco, wildly variable and unpredictable profit margins and net income

Quantity supplied is dictated by OPEC cartel agreements

No practical power for Aramco to choose their own production output

Net income average of ~$100 billion in 2017-2022

270 billion barrels of estimated oil reserves

Major geopolitical risks with respect to security of wells, refineries and distribution networks

Saudi diplomatic relations are very poor with Iran, with Israel and with both nations’ allies and related paramilitary groups

“Saudi Arabia oil facilities ablaze after drone strikes”

“Saudi Aramco Fuel Depot Hit as Drone Attacks Escalate”

Middle East region in general still struggling to achieve peace and harmony

Oil and gas industry is facing shrinking long-term demand with inevitable decline towards extinction and zero hope of salvation

“Peak Oil” may have already occurred around 2019-2022 at 100 million barrels per day

Only time will tell, but for now it looks like it is so

International Energy Agency Oil Market Report for August 2022

If true, Peak Oil will have happened because of a terminal decline of demand (shockingly enough), instead of terminal decline of supply as most people have been worried about for decades

Many governments around the world are now enacting policies either mandating or heavily incentivizing the transition away from fossil fuels to clean, sustainable energy

Natural gas electricity generation and indoor heating are facing immense cost pressures from solar, wind, batteries and heat pumps which get steadily cheaper every year and have been passing the cost-parity threshold in more and more markets worldwide

On the plus side, Aramco has the world’s lowest cost of production (many fields producing at around $10/barrel) which makes for strong gross margins even in down years, so Aramco is likely to be the final survivor of the fossil fuel industry collapse

Severe environmental, social and governance problems, by far the worst of any leading large company

Responsible for more environmental damage than any other single company on Earth

98.5% of equity owned by Saudi Arabian government

One of the last remaining absolute monarchies on this planet

Strict theocracy featuring their own version of Sharia law

Flagrant oppression of women, Shia muslims, anyone who isn’t heterosexual, and several other marginalized demographics

Support for violent terrorists

Abstention from voting on United Nations Universal Declaration of Human Rights, claiming supremacy of Sharia

In 2020 Saudi Arabia’s bid was rejected to retain their seat on the 47-member UN Human Rights Council

Decapitation of dissenting journalists

Allowance of vast swaths of the population of their nation to live in crippling poverty while the Saudi royal family lives in luxurious palaces and parties on their private jumbo jets and humongous yachts

Microsoft

Microsoft Revenue

Microsoft Earnings per Share

Microsoft Gross, Operating and Net Margin

Microsoft Notes

Diverse, balanced product portfolio

Azure, Windows, Dynamics, Teams, Office, LinkedIn, Xbox, Bing, Surface, HoloLens, Minecraft, etc.

Overall theme is expansion of personal computing and giving individuals and organizations power to do more

No single segment dominates

One of the strongest, oldest and most mature software companies in the world

Took an early first-mover advantage in personal computing software, starting with a BASIC interpreter for the Altair 8800 in 1975, and ran with it to develop a high-tech empire over the subsequent five decades

Net income $75 billion (trailing twelve months)

Healthy revenue and earnings growth trend, but nothing mindblowing

Revenue

In last 5 years: Doubled, 15% CAGR

In last 12 years: Tripled, 10% CAGR

Net income

In last 5 years: Tripled, 25% CAGR

2011-2016: Stagnant, 0% CAGR

I live in Seattle and personally have a sample of n = ~100 friends and acquaintances who are Microsoft software engineers as well as a few managers In my sample:

100% of subjects are smart

0% of subjects exhibit any true passion or excitement for their jobs, and mostly are attracted by the high pay and relatively easy, low-stress workload compared to other lucrative careers or other tech companies like Amazon

Not a perfectly scientific sample, probably biased, but still roughly indicative

Slow and bureaucratic

42% operating margin with steady increase up from 30% six years ago

Alphabet

Alphabet Revenue by Segment

Alphabet Revenue

Alphabet Earnings per Share

Alphabet Gross, Operating and Net Margin

Alphabet Notes

Google dominates internet search and YouTube dominates personal video/search

Due to platform effects, economies of scale and data-hungry nature of machine learning, this dominance is likely to continue for the foreseeable future

Strong portfolio of other top-notch freemium software products

Maps, Docs, Android, Chrome, Gmail, etc.

Google Cloud is growing fast, ~40% year-over-year 2022 vs. 2021

Strong contender for #1 artificial intelligence/machine learning organization in the world

Software and computer engineering talent magnet

Net income of $67 billion (trailing twelve months)

$75 billion in 2021 before 2022 decline

Healthy revenue and earnings growth trend, but nothing mindblowing

Revenue

In last 2.5 years: Doubled, 33% CAGR

In last 5 years: Up 2.8x, 23% CAGR

In last 10 years: Up 6.5x, 21% CAGR

Net income

In last 2 years: Up 2.3x, 25% CAGR

2015-2020: Up 2.2x, 17% CAGR

Almost all money comes from Alphabet’s strong platform and tools facilitating advertising for just about anyone who will pay for it

Amazon

Amazon Revenue

Amazon Earnings per Share

Amazon Gross, Operating and Net Margin

Amazon Notes

Amazon Web Services (AWS) is a beast

The world’s leading cloud computing service provider

Amazon basically invented the modern version of cloud computing in the early 2000s, probably circa 2006

~30% year-over-year AWS revenue growth 2022 vs 2021

~50% YoY AWS operating income growth to $12 billion for 1H ‘22

Cloud computing’s long-term TAM is nearly impossible to estimate accurately, but it’s almost certain to continue growing alongside the general economy as well as the growth of digitization and the Internet of Things

Amazon.com is the undisputed global champion in the online retail sector, but with weak profit margins thus far in the story, and consumer retail is highly cyclical in general

Net income

$12 billion (trailing twelve months as of Q2 ‘22)

$33 billion in 2021

Aggressive investments in growth are depressing net income now, but may pay off big in the future

Operating cash flow (TTM) has been as high as $59 billion as of Q2 ‘21

Amazon is gobbling up rights to expensive entertainment content, investing big in AWS infrastructure, expanding footprint of distribution and brick-and-mortar stores, and more

Rivian investment had major recent effect, per Amazon Q4 ‘21 report and Q2 ‘22

“Fourth quarter 2021 net income includes a pre-tax valuation gain of $11.8 billion included in non-operating income from our common stock investment in Rivian Automotive, Inc., which completed an initial public offering in November.”

“Second quarter 2022 net loss includes a pre-tax valuation loss of $3.9 billion included in non-operating expense from our common stock investment in Rivian Automotive, Inc.”

Humongous operating expenses, which have been exponentially growing at 30% per year with no end in sight, and were in 2021:

$75 billion for order fulfillment

$56 billion for “Technology and Content”

This is the closest thing Amazon reports that could be called R&D; check 2021 10-K page 26 for full definition

$41 billion for marketing, general and administrative

$173 billion combined total for these three categories

Serious exposure to uncontrollable cost pressures, especially for fuel and other transportation expenses

Exhibited by first-half 2022 net income going negative

Overall gross margin % in low 40s, but this is with order fulfillment costs counted as operating expenses instead of COGS

Operating margin more like 4-6%

Margins have been steadily improving for years

Heavy price competition in online retail segment and moderate threat from Microsoft Azure and other players in cloud services

Growth trends before the recent slowdown in the last year:

Revenue: 30% per year

Earnings per share: 80% per year

Operating Income: 80% per year

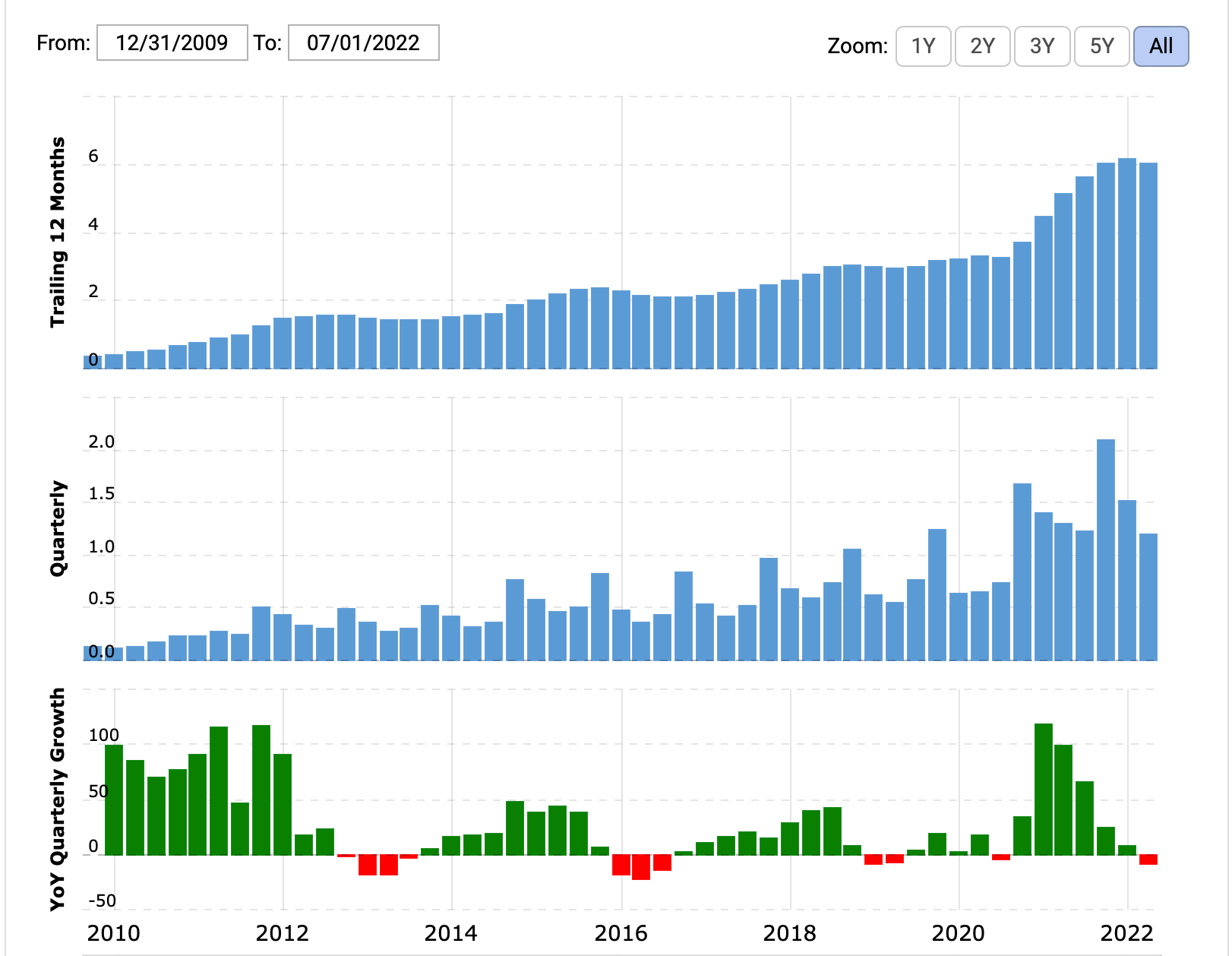

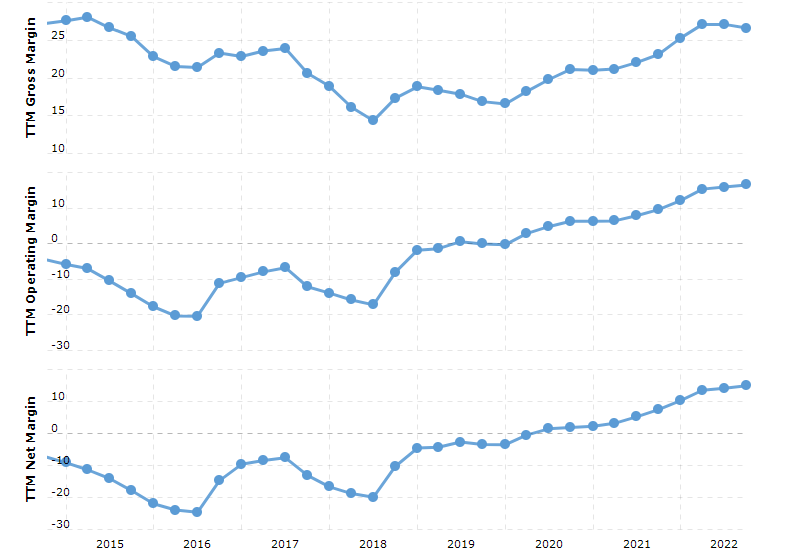

Tesla

Tesla Supercharged Cash Flow and Earnings Growth As Sole Major Automaker that Hasn’t Contracted Since 2019

Tesla Revenue

Tesla Earnings per Share

Tesla Gross, Operating and Net Margin

Tesla Notes

$7 billion total annual operating expenses which have plateaued despite aggressive growth

Breakeven scale surpassed in 2020 and now extreme operating leverage is kicking in hard, and as sales volume skyrockets this effect will make a huge impact on operating margins in the next six quarters or so

Lean operating structure de-risks business in case of severe recession or production disruption

Q2 2022 demonstrated this advantage, with $0.6 billion free cash flow despite Shanghai government lockdowns and uninterrupted overall capital expenditures

Strict prohibition on bureaucracy, boring PowerPoint presentations, information silos, useless middle managers, useless meetings and other common forms of corporate waste

Homegrown enterprise software drives incredible efficiency and extensive digital self-management, with increasing leverage as Tesla scales up

60% compound annual growth rate of vehicle production for the past decade; 10x increase every five years

Tesla has constantly guided for 50%+ growth to continue for foreseeable future

Official target of 20 million vehicles sold in 2030

Approximately current output VW Group and Toyota Motor Co combined

Demand is out of control, with multi-month or multi-year order backlogs for every major product in the catalog

Despite high prices

Despite current general lack of public awareness of the value proposition of Tesla products

~30% automotive gross margins in 2022

Zach Kirkhorn, Master of Coin, announced this on the Q3 2022 conference call

Operating margin is one of our best yet, with improvements in operating leverage. However, Austin and Berlin ramp costs weighed on our margins, particularly if you compare it to Q1. Removing regulatory credits and Austin and Berlin, our operating margins would have been our strongest yet and auto gross margin would have been nearly 30%.

This is more indicative of what Tesla’s baseline margins for mature factories are in the current operating environment, because low-rate initial production inherently comes with worse unit economics than mature volume production

This 30% margin is with the previous generation of factories. Berlin and Austin are designed with

More advanced industrial engineering

Simpler production lines with hundreds of eliminated robots and manual process operations as well

Significantly improved ergonomics and access in General Assembly due to building the seats and a bunch of other stuff directly on top of the battery pack before sandwiching with the upper structure of the car

Major price increases of thousands of dollars per car from March and April this year have not yet come into effect for deliveries due to the extreme order backlog

Inflationary pressures on raw materials, logistics and parts are coming down and management has guided that Q3 was roughly the peak

Numerous concrete reasons to expect rise to around 40% in coming years

20 million vehicles per year at conservative $10k net profit per vehicle is $200 billion which at a conservative 15 P/E ratio would imply a valuation of $3 trillion

4x today’s market cap

Plenty of room for upside on these estimates

Total global auto market is likely to be around 100 million in 2030

Current annualized run rate approximately 1.8 million

It’s almost 2023 so the key question for making 20 million in 2030 is whether Tesla can continue to scale vehicle manufacturing for 7 years at about a 40% or more exponential growth rate

1.8 million vehicles * 1.40^7 = 19 million vehicles run rate at beginning of 2030 with moderate growth in 2030 to raise average to 20 million

There are over a billion ICEVs in the global fleet to replace and 20 million is only about 2% of the fleet per year

Tesla roughly estimates 300 Terawatt-hours (TWh) worth of batteries are needed to transition all of human civilization to renewables and batteries, whereas total global annual battery production is currently around 1,000x less than the overall TAM

$2.6 billion research and development expenses in 2021

Tesla is arguably the most prolific technology researcher and developer in the history of human civilization and is investing as fast as productively possible, but nevertheless is spending mere pocket change doing it all

$12.7 billion total cumulative capital expenditures from Q2 ‘20 through Q2 ‘22

During this period, gigafactories in Berlin and Texas were constructed while production from Fremont and Shanghai nearly tripled, and Tesla also of course had plenty of capital expenditures not related to vehicle capacity expansion

Roughly 100%+ IRR expected for construction investments in Berlin and Texas

The factories only cost maybe $5 billion each to build and will earn at least that much operating cash flow each year

$0.063 billion total debt not related to vehicle and energy product financing

Growth is now being funded solely via operating cash flow, not stock sales nor balance sheet leverage

Greatly reduces risk

Model Y on pace to take the “Best-Selling Car Ever” crown from Toyota Corolla sometime in 2023

Despite having price tag more than 2x higher, no Apple CarPlay nor Android Auto yet, only 5 paint color options, no paid advertising, less brand history, etc.

Production capacity, not demand, is the current bottleneck but Berlin and Texas will probably add at least half a million Ys to supply next year to supplement the growing output from Fremont and Shanghai

$21 billion cash and cash equivalents at end of Q3 ‘22

$9 billion total free cash flow for Q4 ‘21 through Q3 ‘22

$3.3 billion of which came in Q3 ‘22 itself

Growing quickly

$0 paid advertising expenditure as opposed to car industry average of roughly $1k per car

Loyal, cult-like fanbase locked into seamlessly integrated software and hardware ecosystem, many of whom won’t even consider buying from competitors

Raving word-of-mouth marketing from almost religious-like customer evangelism, the likes of which no company in any major industry has ever enjoyed before

CEO/Technoking is an extremely famous attention magnet (not always for good reasons, but hey, publicity is publicity)

Case in point: Boring Company “Burnt Hair” perfume sold out of 30,000 limited-edition bottles of within a week of Elon Musk first announcing it on Twitter

When other car companies advertise their own EVs, Tesla’s sales increase

Hertz has been advertising Teslas with Tom Brady “Let’s Go!” campaign

5 days worth of completed vehicles in inventory on average between the time vehicles leave the factory and the customer accepting delivery

Cars delivered directly to customer without sitting uselessly in parking lots collecting dirt and bird droppings while consuming working capital

Industry average pre-COVID, including dealership portion of value chain, is closer to 3 months worth of inventory

About 18x more inventory than Tesla has

Just-in-time logistics is massive boost to cash conversion cycle

Especially because Tesla gets paid for delivered cars about two months before having to pay suppliers for the parts

Biggest and best EV charging network in the world by a wide margin

39,000 Supercharger stalls globally

Adding about 10,000 more per year right now

In process of opening up to other brands of EVs, which will expose customers of other companies to:

Tesla branding

Downloading the Tesla app and making an accounr

Casual encounters with Tesla owners

Seeing how much faster and smoother the charging experience is for Tesla vehicles

Technology lead over competition that is immense and rapidly growing

Magnet for ambitious genius engineers

Employees voluntarily show up for 70- to 100-hour, hardcore work weeks because the job matters to them, is often fun and exciting, and fulfills their deep human desire for feelings of creativity, camaraderie, purpose and mission

Led by Elon Musk since 2007

Holds the best entrepreneurial and engineering leadership track record of all time by a wide margin

Has an almost pathological inability to give up on goals

“I don’t ever give up. I mean, I’d have to be dead or completely incapacitated.”

Literally willing to spend the night on the floor in the factory in a sleeping bag when the situation demands it

“Nobody wants to bleed for the prince in the palace”

Does this job because he thinks it’s important for its own sake, despite him being able to live a leisurely life of extravagant luxury, fame, exclusive parties, beautiful women and private islands

Has a sense of humor, mocks himself in public, and is not a stuffy, uptight businessman; had his official job title changed to “Technoking” as a joke

Takes no salary; 100% at-risk stock options are his only compensation

Unclear if a new compensation plan to replace 2018 package is even in the works at this time

Says and does things that are controversial

Sometimes broadcasts poorly informed opinions on topics outside his areas of expertise

Tends to have trouble reading the room from time to time

Deep vertical integration

Growing, hurricane-force tailward from governmental and societal support

Urgent need to transition world to clean, sustainable energy

Urgent need to reduce funding going to tyrannical regimes such as those of Russia, Iran, Saudi Arabia and Venezuela

Inflation Reduction Act clean energy subsidies will in 2023 begin to provide enormous additional profits in the USA, Tesla’s #1 market

Worldwide, many policymakers are setting dates for banning sales of new ICEVs in the 2030s, such as:

EU 2035

California 2035

UK 2030

China 2035 (at least 50% gas/diesel-free, rest must be hybrid)

Symbiosis with SpaceX

Free-flowing transfer of technology, ideas and even employees

Strong co-branding such as SpaceX livestream showing Model X transporting astronauts to launch pad with final photo opportunity while saying goodbye to their loved ones in heartwarming moment of peak emotional intensity

If this is not *perfect* product placement, then I don’t know what is

Massive additional upside potential if any of the following works out:

Autonomous driving

Useful humanoid robot

Solar roof

Virtual power plants, Autobidder and other electricity services

Unknown secret projects

Summary

Apple, Aramco, Microsoft, Alphabet and Amazon are extremely strong companies. Obviously, this is why they are all valued at more than $1 trillion each.

However, Tesla has by far the best:

Revenue and earnings per share growth

Total addressable market and long-term growth potential

Debt

Operating leverage

Gross margins with the strongest improvement trend, roughly tied with Apple

I’m modeling for Tesla to sail past even Apple’s net income approximately three years from now, while still furiously growing.

Right now my Tesla model for 2023 has:

Deliveries of 2.8 million cars

Gross profit per car rising into a range around $20k-$25k as Tesla improves unit economics on both the revenue and cost sides of the equation

OpEx under $8B

Profit bonanza of $58 billion GAAP net income, although the range of probable outcomes is roughly $30B to $80B.

My intuition still doesn’t want to believe it, but I derived each number independently of the others as best I could based on rigorous economic and engineering analysis and I've spent all year trying to figure out if I've lost my mind, yet I keep getting similar results. More detail coming in future Global Optimization posts…

So in my estimation there really is no one and nothing stopping Tesla from becoming the world's most highly valued company within the next two years solely based on the fundamentals of their automotive business unit, not even counting any expectations for increased Full Self-Driving revenue or Tesla Energy profits beyond a few billion per year. I think TSLA is obscenely underpriced at $200 and people selling now are likely to regret the decision for the rest of their lives. When Tesla gets to Microsoft- and Alphabet-level quarterly earnings by around 2024 and is still showing growth above 50% per year, it's hard to see Tesla not shooting to #1 at around $3 trillion market cap and $800+ share price.

I am about 99.9% all-in on Tesla via TSLA stock and call options. These are notes for my model that I’m sharing. I fully believe what I have written and I’ve put all of my money where my mouth is, but this is not advice regarding your personal investment or financial decisions. I'm not a certified professional investment or financial advisor and even if I were one, broad buying or selling advice would be inappropriate because there are so many variables to take into consideration such as your goals, risk tolerance, financial outlook, income, age, tax situation, dependents, and so on. Make your own choices. I hope one of those choices is to share this article with everyone you know, but that’s up to you. Thanks for reading.

Great work as usual Gigapress. You never disappoint. I look forward to future installments.

I would humbly recommend adding a donation option for those who’d like to chip in some $ but maybe don’t want to commit to an ongoing membership.

Excellent analysis with supporting data, thanks Gigapress.

I personally believe the master FUDsters are very aware of how huge Tesla/ SpaceX (and now Twitter most likely) are in reality now and how they will be even more so in the future.

Therein lies Tesla's possible future black swan. Corporate America (or those who really control the US) won't just stand there letting Elon grow too much in power, for the good of the world and the US. They want to continue tightening their grip on the US (and a lot of the rest of the world).

Right now they are happy fleecing Joe Public manipulating the heck out of TSLA, with the SEC and most of the US government helping out.

I won't speculate much re what that black swan could be now; some comments I left on TMC went w/o much reaction. (Practical note: I would keep a safe portion, say 20% of my investments outside TSLA, just in case).

Some tidbits of side information:

The all in approach to TSLA was good till about 2020 - afterwards it's a lot less clearcut.

For example getting into BTC was excellent till about 2017 - once GS (Goldman Sachs) entered the fray and started a BTC fund, it was game over. WS was then able to manipulate BTC's price and perception, with the SEC/ Fed policies.

Little factoid, re Ukraine: the US gov prediction at the time of the invasion was that Ukraine would fold (they were surprised Zelensky refused their offer to flee the capital).

One nagging possibility is that it was all going according to plan. Creating a huge conflict in Europe was the perfect distraction for the manufactured Covid crisis imploding on itself, and at the same time also to crash the markets, Tesla included.

That backfired big time as Ukraine proved it could hold its own against Russia, and the ensuing accelerated push for an alternative to fossil fuels.

The US big push for alternatives will help Tesla no doubt, but in reality will be helping much more the ICE, and I'm pretty sure the oil & gas industry as well.